May 1, 2026

Flow of Funds Statement and Its Role in M&A Deals

With global cross-border mid-market M&A reaching €180 (appox. $215 USD) billion in 2024, a Flow of Funds Statement is essential for accurate price true-ups.

Such a statement clearly identifies how capital moves within a business over a defined period.

What is a Flow of Funds Statement?

A Flow of Funds Statement explains how a company generated and used funds over a period by reconciling changes in working capital.

What Makes it Different from Other Financial Statements?

A Balance Sheet is a point-in-time screenshot, an Income Statement explains profitability over a period, and a Cash Flow Statement tracks only cash and cash equivalents.

A Flow of Funds, on the other hand, is working capital shifted between two dates, and what financing and investment moves drove that change.

Key Components of a Flow of Funds Statement

There are two main components to a Flow of Funds Statement:

- Sources of Funds

- Uses of Funds

Sources of Funds

These are inflows. They include all areas from which the business got its capital during the period.

For example:

- Funds from Operations: This is what the company generates internally.

- Sales of Fixed Assets or Investments: Proceeds from selling investments to free up cash.

- Equity Raised or Long-term Debt Issued: New shares, bonds, or loans.

- Decrease in Working Capital: If current assets drop or current liabilities grow.

Together, these make up the inflow of the company’s sources of funds over this period.

Uses of Funds

These are outflows. These are areas where the company has allocated or spent capital.

For example:

- Capital Expenditures: Purchasing property, new equipment, or long-term assets.

- Debt Repayment: Paying down bonds, loans, or other obligations.

- Dividend/Distribution Payments: Paying shareholders either through dividends or buybacks.

Merged together, these give you the uses of the funds for a Flow of Funds Statement.

Why the Flow of Funds Statement Is Critical in M&A

An M&A Flow of Funds Statement can be beneficial. It can help break down the movement of capital so buyers and sellers can validate how money is generated, deployed, and distributed.

- Due Diligence Transparency: Confirms whether the business funds operations organically or relies on debts, temporary financing, or equity injections.

- Working Capital Accuracy: Identifies abnormal swings in receivables, payables, or inventory that could distort purchase price adjustments.

- Capital Structure Clarity: Documents new borrowings, refinancings, or owner distributions that affect leverage and closing proceeds.

- Earnings Quality Validation: Separates recurring operational performance from one-time inflows or asset sales.

- Closing Execution Precision: Serves as the final schedule of debt payoff, fees, escrows, and seller proceeds.

This is why adding a Flow of Funds Statement to the M&A deal cycle is so important. It can help uncover risk and validate wins.

How to Prepare a Flow of Funds Statement

If you want to prepare your own Flow of Funds Statement, the following guide will help:

- Step 1: Gather Balance Sheets for Two Periods. Use comparative balance sheets to identify all line-item changes, like one from 2024 and another from 2025.

- Step 2: Calculate Changes in Working Capital. Measure increases or decreases in current assets and current liabilities.

- Step 3: Identify Sources of Funds. Classify inflows such as operating profits, new debt, equity issuance, or asset sales.

- Step 4: Identify Uses of Funds. Record outflows, including capital expenditures, debt repayments, dividends, or acquisitions.

- Step 5: Classify Long-Term Financing Activities. Separate structural financing changes (like new loans or refinancing) from operational movements.

- Step 6: Total Sources and Total Uses. Add all the identified sources and double-check the data before calculating the net change.

- Step 7: Calculate Net Change in Funds (Sources − Uses). Determine whether funds increased or decreased over the period.

- Step 8: Reconcile Opening and Closing Balances. Confirm that the net change bridges the opening funds position to the closing funds position.

- Step 9: Cross-Check with the Cash Flow and Income Statement. Validate consistency and ensure that no operational or financing activity has been overseen.

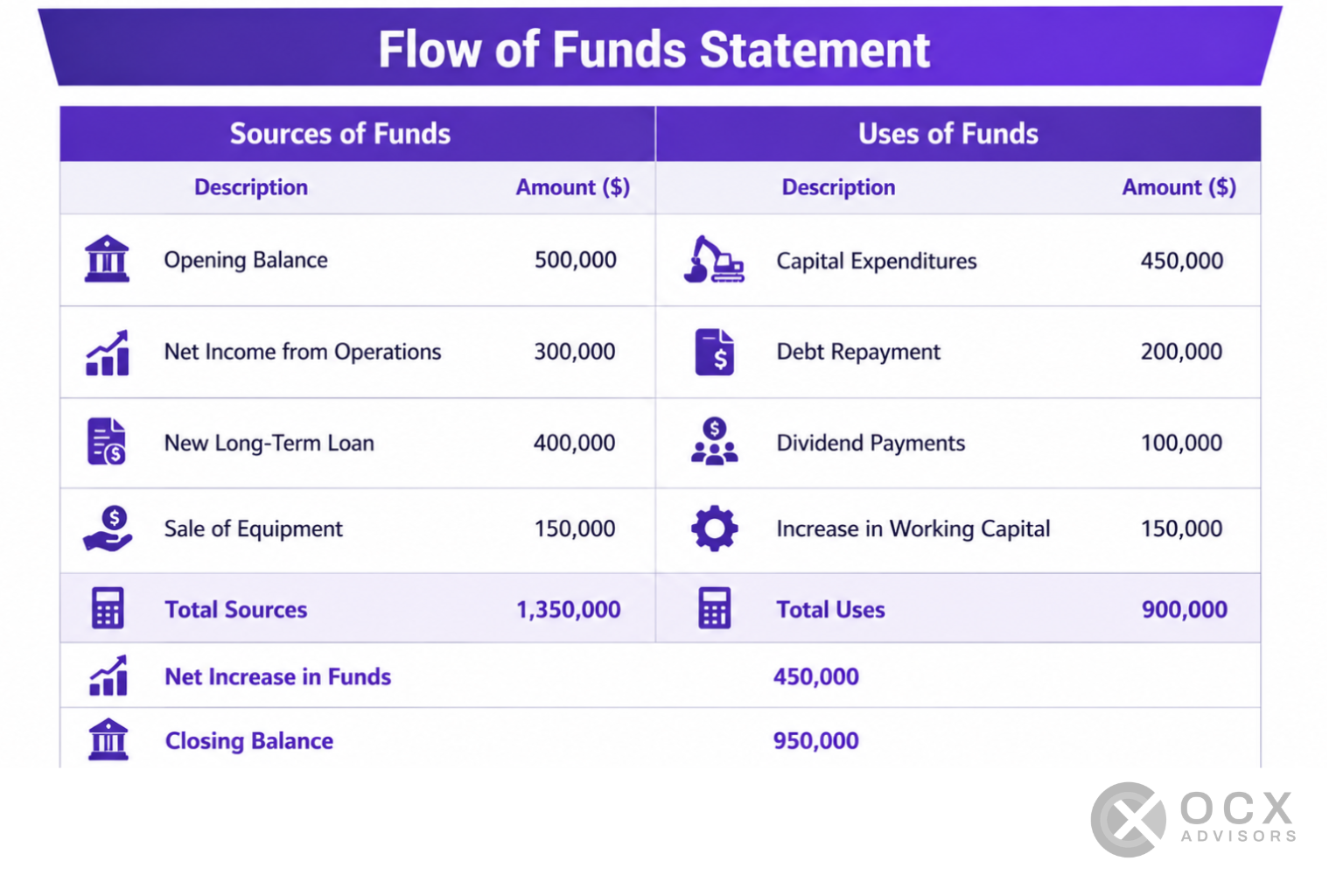

Flow of Funds Statement Example

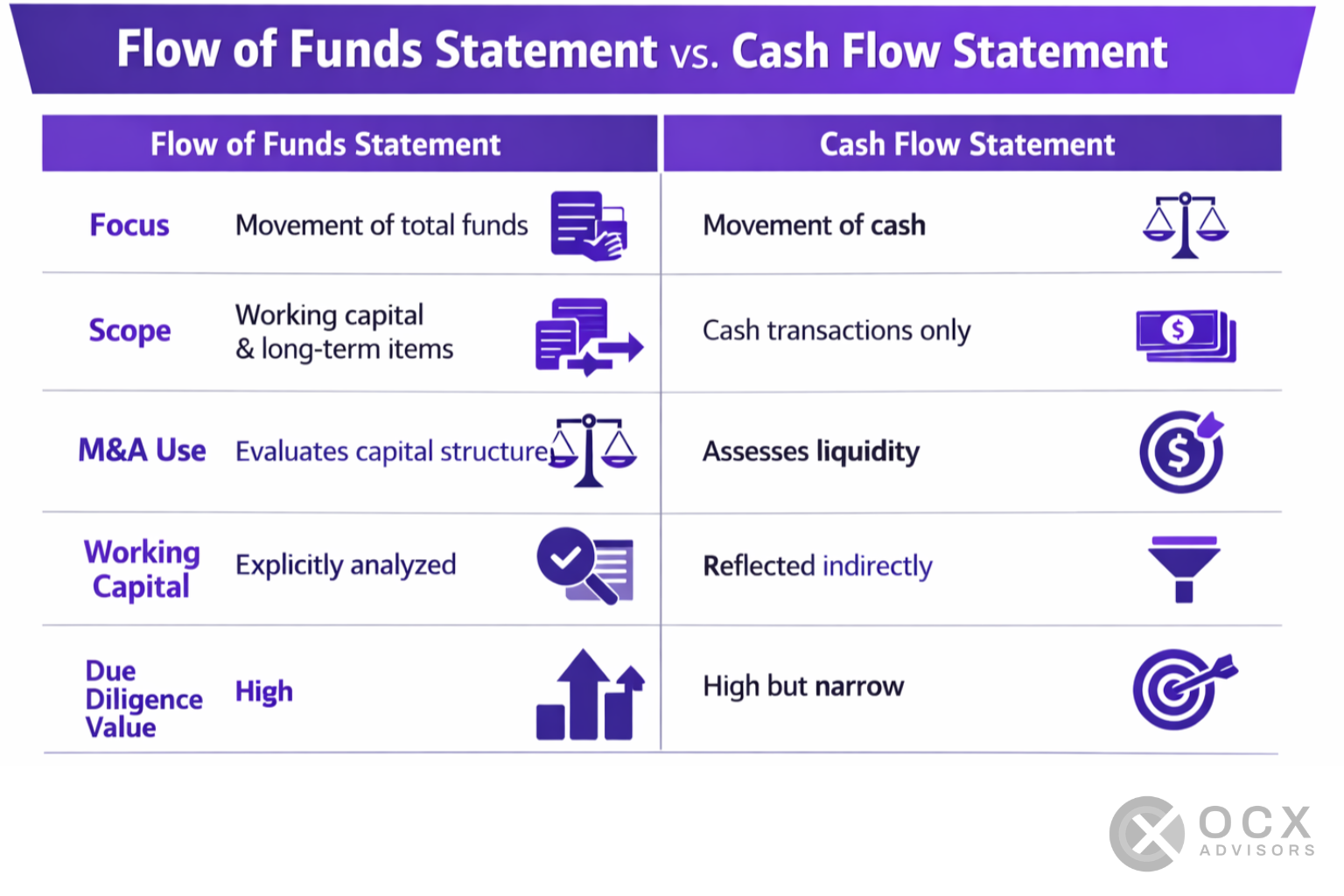

Flow of Funds vs Cash Flow in M&A Context

Flow of Funds and Cash Flow are usually mixed up in the context of M&A. However, there are some important nuances that can’t be overlooked.

Limitations of a Flow of Funds Statement

A Flow of Funds Statement can be a strong diagnostic tool. However, it should be read alongside the “core” financial statements and deal schedules.

Remember, it’s based on historical balance sheet data. As a result, it doesn’t capture events that occur after the reporting period, for example, new operational disruptions, post-period liabilities, or new financing.

Including this, it doesn’t directly measure profitability. This is the role of an income statement.

It may also overlook strategic, non-cash factors, such as contractual risk and management changes.

Plus, for non-financial stakeholders, a Flow of Funds statement can be hard to interpret, and on its own, it doesn’t predict future performance.

Conclusion

A Flow of Funds Statement offers a clear overview of how capital is generated, allocated, and structured within a business.

When used correctly, for example, with a balance sheet, income statement, and cash flow statement, it can boost the strength of due diligence, improve purchasing price accuracy, and support cleaner deal execution.

If you’re buying or selling a business, feel free to contact a helpful representative at OCX Advisors today.

We can help you acquire time, growth, and unrealized profits today.